Owning a rental property can be a smart way to generate long-term income—but like any investment, it comes with risks. Unexpected damage, legal issues, or income loss can turn a good opportunity into a costly mistake. That’s why rental property home insurance, also known as landlord insurance, is so important. It helps protect your property, your finances, and your peace of mind.

Whether you’re renting out a single-family home or managing multiple units, understanding how this insurance works can help you avoid major headaches. In this post, we’ll walk you through what rental property insurance covers, what it doesn’t, and how to choose the right policy for your needs.

What Makes Rental Property Insurance Different?

Unlike standard homeowners insurance, which is designed for owner-occupied homes, rental property home insurance covers the risks that come with having tenants. When someone else is living in your property, there’s simply more that can go wrong—from accidental damage to liability claims.

This type of insurance usually includes coverage for the structure of the property itself, liability protection in case someone gets injured, and compensation for lost rental income if the property becomes uninhabitable due to a covered event. Some policies also protect items like kitchen appliances or furniture that you, as the landlord, provide with the rental.

It’s not just about covering big disasters—it’s about having a safety net that allows you to recover and keep going if something unexpected happens.

Why Landlords Need This Protection

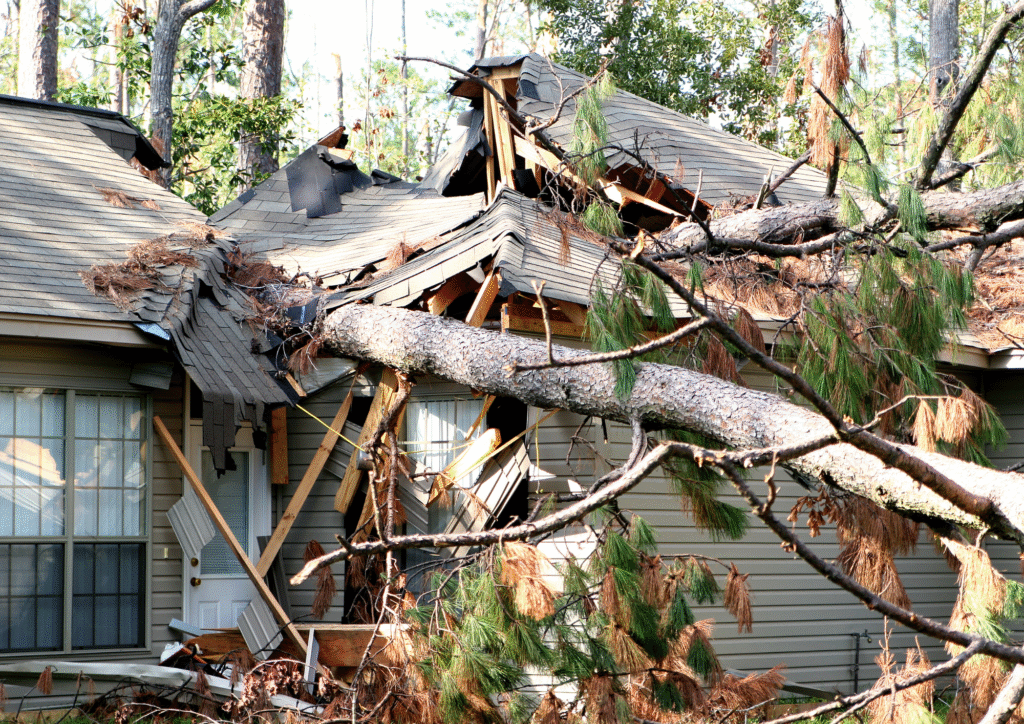

Imagine a pipe bursts in your rental unit and the damage forces your tenant to move out. Not only are you responsible for the repairs, but you also lose rental income in the meantime. Or worse, someone slips and falls on the front steps and decides to sue. Would you be financially prepared to handle it?

That’s where rental property insurance steps in. It offers financial protection against property damage, legal claims, and income loss—things that can quickly add up and affect your bottom line. If you rely on your rental income to help pay a mortgage, this kind of coverage is especially important. It ensures that one incident doesn’t throw off your entire financial plan.

What’s Typically Covered

Here’s a quick look at some of the core protections you can expect from a standard rental property insurance policy:

Property damage: Covers physical damage to the structure caused by events like fire, wind, hail, or vandalism.

Liability protection: Helps cover legal expenses and medical costs if someone is injured on your property and you’re found responsible.

Other coverages, like loss of rental income or landlord’s personal property (like a refrigerator you provide), are often available as add-ons. Depending on where your property is located, you might also want to consider separate flood or earthquake insurance.

Factors That Affect Your Premium

The cost of rental property home insurance can vary based on several factors. Location is one of the biggest ones. If your rental is in an area that’s prone to flooding, hurricanes, or wildfires, you’ll likely pay more due to the higher risk of damage. The age and condition of the property also play a role—older buildings with outdated systems may lead to higher premiums unless they’ve been updated or well maintained.

The type of tenants you rent to can also influence your rate. For example, properties rented to students or short-term tenants may carry more risk in the eyes of insurers. On the other hand, long-term tenants with a clean rental history may help keep costs down. Features like smoke detectors, fire sprinklers, and security systems can qualify you for discounts. And of course, your own claim history matters—fewer past claims usually means better pricing.

What Rental Property Insurance Doesn’t Cover

Even a solid policy has limitations, so it’s important to know what’s not covered. One common exclusion is flood or earthquake damage—those typically require a separate policy. Another is intentional damage caused by tenants or long periods where the property is vacant. If your rental sits empty for too long, some protections may pause unless you’ve added vacancy coverage.

Wear and tear, pest infestations, and routine maintenance issues also aren’t covered. As the property owner, you’re expected to keep the home in safe, working condition. If something breaks down from old age or neglect, that’s on you—not the insurance company.

How to Choose the Right Provider

Not all insurance companies are created equal. When choosing coverage, look for a provider that not only offers competitive pricing, but also has a good reputation for handling claims fairly and quickly. Make sure the policy terms are clear and that the coverage is flexible enough to match your specific situation.

At Premium Insurance Group (PIG), we take the time to explain the details, answer your questions, and help you customize a policy that fits. Our team knows that no two properties are alike, and your insurance shouldn’t be one-size-fits-all either.

Smart Ways to Save on Your Policy

If you want to lower your insurance costs without sacrificing protection, here are two easy strategies:

Bundle your policies: Insuring your rental property with the same company that covers your home or auto can lead to discounts.

Raise your deductible: Choosing a higher deductible can reduce your premium—but make sure it’s an amount you can handle if you need to file a claim.

Staying proactive with maintenance, installing safety features, and reviewing your policy each year can also lead to savings. Sometimes, simply updating your insurer on recent upgrades or repairs can unlock better rates.

Why Policy Reviews Matter

Once you have insurance in place, don’t just forget about it. Life changes, properties evolve, and insurance needs shift over time. You should review your policy once a year or whenever you make changes to the property—like renovations, upgrades, or switching tenant types. Keeping your coverage up to date helps ensure you’re not overpaying or underinsured.

Also, if you start earning more from the property or take on new risks, your existing policy might not be enough anymore. That’s why ongoing conversations with your insurance agent are so important. It’s not just about buying a policy—it’s about managing it well.

What to Expect When Filing a Claim

If something happens and you need to use your insurance, the first step is to report the issue right away. Document everything—photos, videos, receipts—and be prepared to explain what happened. An adjuster may visit the property to assess the damage. If you disagree with their evaluation, you can negotiate or present additional documentation to support your claim.

Keep records of all repair costs and communication with your insurer. And once the claim is resolved, take time to evaluate what went well and whether you need to adjust your policy moving forward.

Final Thoughts from Hemelyh

“Owning a rental property means taking care of more than just bricks and walls—it means protecting your financial future. The right insurance gives you peace of mind and the freedom to grow your investment without fear. At PIG, we help you understand your policy from the inside out, so you can make smart decisions every step of the way.”

– Hemelyh, CEO of Premium Insurance Group

Need help reviewing your rental property coverage?

Let’s go over it together. Schedule a free consultation with our team and find out if your investment is fully protected.